How to Create Risk-Free Option Positions

A breakdown of my favorite options trading strategy.

This year, I’ve talked about the “risk-free call spread” positions that I’ve created numerous times in many of my options trading videos this year.

Today I’ll break down the strategy and explain how it:

1) Reduces/removes all of your risk.

2) Alleviates your margin requirement/increases your account’s cash position (which you can allocate to new trades or withdraw from the account).

3) Can be strategically traded in and out of to potentially increase the position’s profitability.

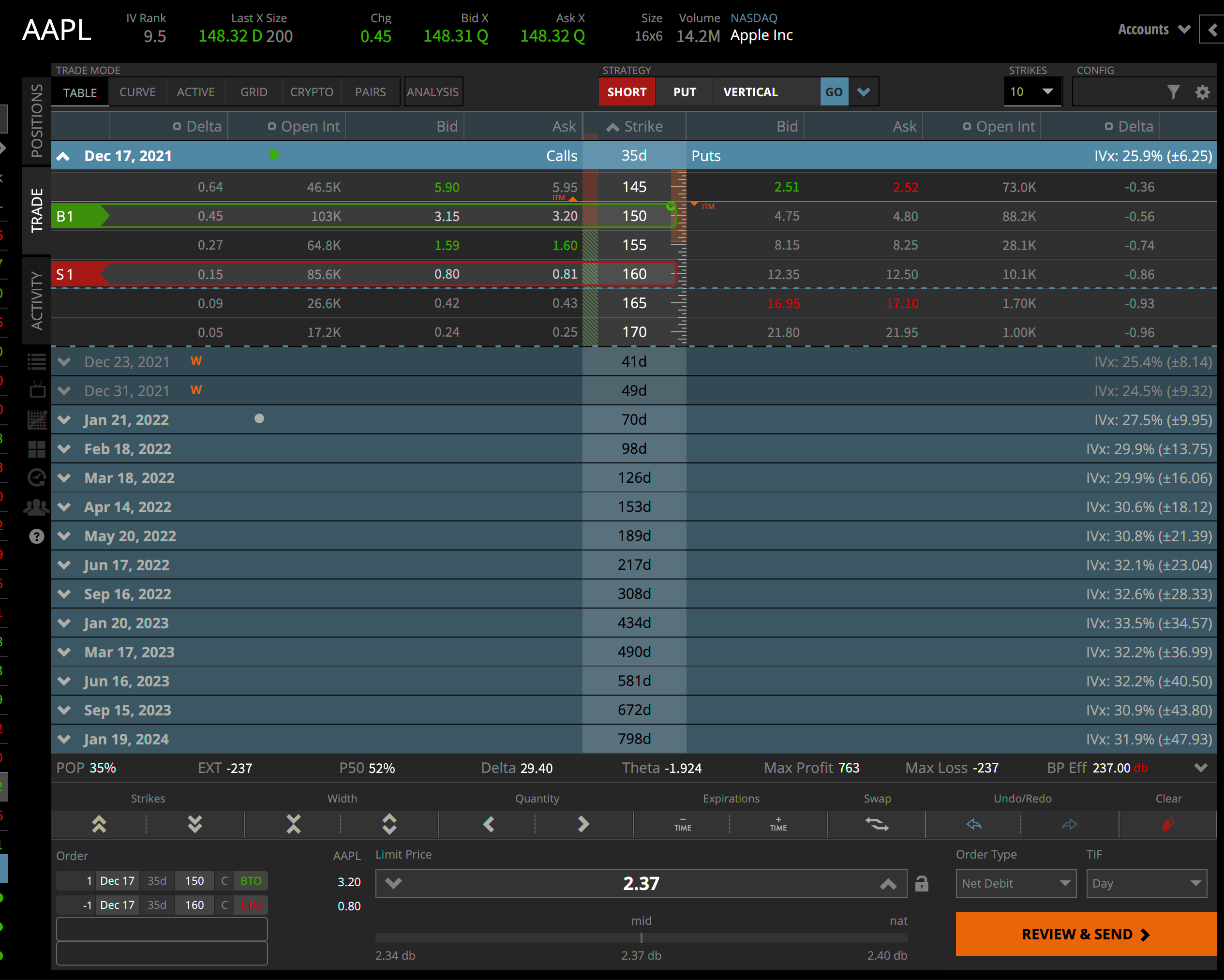

Normal Call Spread Entries

Buying a call spread consists of buying a call option at one strike price and shorting another call option at a higher strike price (same expiration):

When I enter both legs (leg = each strike/option in the trade) of the trade at the same time, I pay more for the call I buy than I receive for the call I short.

In the above example, entering the 150/160 DEC call spread in AAPL costs me $237 because I pay $317 for buying the 150 call and receive $80 for shorting the 160 call.

This means if AAPL is below $150 at expiration, both calls expire worthless.

If both calls expire worthless, I lose $317 on the 150 call and make an $80 profit on the short 160 call. Total loss => $237 => what I paid for the spread.

You will always pay to enter a bull call spread like this when you enter both legs of the trade at the same time because a lower-strike call will always be worth more than a higher-strike call.

Legging Into Trades

What allows me to create a risk-free call spread is “legging into” the trade, which means I create the call spread in two separate transactions at different points in time.

Here’s an example using my TSLA 900/1500 call spread position:

First, the column headers:

DTE => Days to Expiration

Trd Prc => Trade Price (what I paid/received for the option)

Mrk => Market Price (current price of the option)

P/L Open => Profit/Loss since opening the option

D’sOpn => Days Open => Days since entering option.

The first part of the call spread (the long 900 call in JAN 2023) was purchased 415 days ago on September 23rd, 2020:

At the time, TSLA was trading around $380:

So I bought the 900 call expiring in ~850 days when TSLA was around $380/share.

TSLA exploded higher in the coming months, allowing me to enter the second part of the trade on January 8th, 2021. On that day, I shorted the 1500 call in the JAN 2023 expiration for $233, collecting $23,300 into my account:

The timing of this trade was fortunate as I shorted the call at the top of the rally:

Here’s the math up to this point in the trade:

Bought JAN ‘23 900 Call on 9/23/2020 for $10,130

Shorted JAN ‘23 1500 Call on 1/8/2021 for $23,300

Since I paid $10,130 for the 900 call and received $23,300 for shorting the 1500 call, I get the 900/1500 BULL call spread for a credit of $13,170.

Additionally, the trade completely alleviates my margin requirement.

When I initially bought the 900 call for $10,130, my margin requirement was $10,130. When I shorted the 1500 call for $23,300, my account’s option buying power increased by $23,300, effectively pushing my position’s margin requirement to $0 and adding another $13,170 to my account’s cash position/buying power. I can then allocate that money to a new position or withdraw that money from my account.

If TSLA is below $900 when these options expire, the 900 and 1500 calls will be worth zero.

Therefore, I’ll lose $10,130 on the 900 call that I bought and make a $23,300 profit on the 1500 call that I shorted.

Profit => $13,170.

If TSLA is above $1500 at expiration, the 900/1500 call spread will be worth the width of the strikes, or $600, which is $60,000 in actual dollars since we have to multiply the option position’s price by 100.

In that scenario, I could sell the call spread for $60,000, and since I received a $13,170 credit for entering the spread, my total profit would be $73,170.

The position’s expiration payoff graph looks like this:

The position can’t lose.

Of course, it’s not an easy position to create all the time because you need a significant stock price increase after buying a naked call.

Buying a naked call is riskier than purchasing a call spread from the beginning:

Going back to our AAPL call spread from earlier, we can see that just buying the 150 call by itself would cost about $317 instead of $237 for the call spread.

So to create a risk-free call spread, you first have to take more risk than buying a call spread from the beginning because you have to start with a naked call.

Then the stock price has to increase quickly enough so that you can short a higher-strike call for equal to or more than the initial purchase price of the long call.

Timing

When do you take your profitable naked long call and convert it into a risk-free call spread? The sooner you short a higher-strike call to create a risk-free spread, the less attractive the overall position will be.

For example, I purchased the 900 TSLA call for $101.30 when the stock price was $380.

If the stock price increased to $450 and I shorted the 950 call for $101.30, I’d have a $50-wide call spread (900/950 call spread) with no risk.

My max profit would be $5,000 because a $50-wide call spread’s max value is $5,000 (strike width x 100), and I paid a net entry price of $0.

The above call spread is far less attractive than the $600-wide call spread I have for a net credit.

I have a much wider call spread for a net credit because I shorted the 1500 call when TSLA approached $900/share instead of creating the spread when TSLA was at $500 or $600. I waited a long time and saw a massive stock price increase before shorting the 1500 call.

When implementing this strategy, you have to balance:

1) shorting the higher-strike call too soon and creating a narrow spread (smaller profit potential than a wider spread)

2) being too greedy and not shorting a higher-strike call when the stock price does increase.

I got really lucky with my timing of the trade as I did short the 1500 call at the top of the rally into January 2021:

I could have created a risk-free spread much sooner if I had shorted a call above the 900 strike when the stock price was $600, but my short call strike might have been 1200 instead of 1500 (a $300-wide spread instead of a $600-wide spread).

Need a brokerage account? tastyworks is running a limited-time promotion where new customers can get a $500 bonus when funding $10K+.

The JAN ‘23 1200 TSLA calls were trading for about $130 on December 7th, 2020, when TSLA shares were somewhere around $600:

Had I shorted the 1200 call for $130, I’d have the 900/1200 call spread for a $3,000 credit (paid ~$10,000 for the 900 call and received ~$13,000 for the 1200 call).

My advice would be to have a stock price target that triggers the conversion of the long call into a risk-free call spread.

Since this trade was so long ago, I can’t recall why I waited so long to short the 1500 call. I believe it was the first iteration of using this strategy, and I adjusted after TSLA shares went parabolic.

Managing the Short Call

One massive benefit of this strategy is that you can trade in and out of the short call.

If the stock price falls after shorting the call portion of the trade, you can buy back the short call for a profit with the idea being you re-short the call if the stock price begins to rally again.

Here’s the price chart of the JAN ‘23 1500-strike call in TSLA:

The lefthand side of the chart is January 2021, which is where I initially shorted the 1500 call for $233, collecting $23,300.

The chart says I shorted the call at $117.70 because I did buy back the short call and re-short it for $117.70. I didn’t benefit at all because I repurchased it for $117.70 and then re-shorted it a few weeks later for the same price of $117.70. Since the exit/re-entry happened to be at the same price, it’s as if I never closed it (except for realizing a gain). Bad trade.

I changed my mind and ultimately decided I’d rather have the protection of the short call to reduce my position’s risk than try to push my luck timing the market by waiting for another stock price increase (which may not have happened).

The point is, if I shorted the 1500 call for $233, bought it back for $117, then re-shorted it for $150 (a hypothetical example), I’d add another $3,300 to my overall credit:

Paid $10,130 for 900 call

Received 23,300 for 1500 call

Paid $11,700 for 1500 Call

Received $15,000 for 1500 call

= ($23,300 + $15,000) - ($10,130 + $11,700) = $38,300 credits - $21,830 debits = $16,470 Net Credit.

An additional $3,300 in credit compared to the original $13,170 net credit. The downside of buying back the short call with the intention of shorting it again later is that you increase the position’s risk. By buying back the 1500 short call for $11,700, I add $11,700 to the position’s risk.

So you can either hold your risk-free call spread without doing anything, or you can trade in and out of the short call if the stock price collapses after shorting it.

Overall, the strategy gives you a lot of flexibility, reduces/removes your risk, and eliminates your position’s margin requirement/increases your account’s cash position.

I’m running into the word limit on this post so I’ll have to end it here! I hope this post was helpful. Comment below with questions if you have any.

Enjoy your weekend!

-Chris

Dude, you have no idea how much I've learnt from you. You made a video about this TSLA trade a while ago and i was blown away and perplexed that such a tactic is not widely spoken about. Then, I came across someone else who recently did this exact same thing and it encouraged me to give it a shot. I legged into a bull call spread on LCID but my max profit is only $2200 (not like the $60k you legged into haha). Either way, this is by far turning out to be my favorite way to trade stocks that have the potential to move higher. Thanks for the detailed post on the TSLA trade, love it.

Chris if the stock is above both strikes are you exiting the spread before expiration or letting them both expire? If exiting, does the order in which you sell the long call and buy back the short call matter?