How to Learn Options Trading Concepts (Zero to Hero)

Follow this simple framework to master options trading concepts (or anything).

Options trading is a tough subject.

You have long calls, short puts, iron butterflies, gamma scalping, implied volatility, assignment risk, costless collars, etc.

It can be very overwhelming for a beginner.

Let me make you feel better about wherever you are now: when I first started learning about options, I did not think I would ever understand some of the concepts.

“Implied volatility?” Sounds really complicated. I’m not smart enough to understand that.

Over time, I learned the concepts which allowed me to create a YouTube channel helping others to do the same.

The Basic Building Blocks

You don’t need to study 30+ options strategies to learn them all. You just need to know the building blocks.

The first-principles approach to learning options strategies is to learn the building blocks of all strategies: calls and puts.

ALL options strategies consist of either long or short calls/puts.

Therefore, if you master how long calls, short calls, long puts, and short puts work, then you can figure out all of the other options strategies.

Let’s walk through an example.

Calls, Call Spreads, and Butterflies

When you buy a call, you want the stock price to increase as much as possible. Whenever you pay to enter an option/strategy, you want it to have value at expiration.

When you short a call, you don’t want the stock price to increase. Ideally, the stock price is below the short call’s strike at expiration. Whenever you short an option, you want it to be worthless at expiration.

If you get really comfortable with how long calls and short calls perform relative to the stock price, then you are prepared to know what you want out of a long call spread.

Long Call Spread

If you buy a call spread (long call spread), you buy a call and short a call at a higher strike price.

If we combine the basic explanations from above, we can figure out what we want to happen with a long call spread.

Long Call: I want the call to be as valuable as possible at expiration.

Short Call: I want the call to be worthless at expiration.

If I buy a call spread, I want the spread’s value to increase.

Based on the simple explanations above, at what point can I satisfy both goals?

If I want the long call to be as valuable as possible while the short call isn’t valuable at all (at expiration), then that means when I buy a call spread I want the price to go to the short call’s strike price:

Of course, if the stock price goes to infinity, we get the same profit, but the basic understanding of the strategy is that we are both buying a call and shorting another call at a higher strike price.

To have a maximally profitable long call while having a worthless short call, we want the stock price to be at the short call’s strike at expiration.

Short Call Spread

But what about a short call spread?

A short call spread consists of shorting a call option and buying another call option at a higher strike price.

If we again take the simple explanations from above, how do we figure out where we want the stock price to be when shorting a call spread?

Long Call: I want the call to be as valuable as possible at expiration.

Short Call: I want the call to be worthless at expiration.

To figure this out, remember that if we buy a spread, we want the spread’s value to increase. If we short a spread, we want the spread’s value to go to zero.

So if I have a short call and a long call, at what stock price do both options go to zero at expiration?

The answer is the stock price needs to be below both strike prices because a call option will have value if the stock price > call strike at expiration.

To break down what we’ve covered so far:

Long Call: I want the call to be as valuable as possible at expiration.

Short Call: I want the call to be worthless at expiration.

If I buy a call spread, I want the spread to have value at expiration. At what point can I maximize the above conditions?

Answer: I want the stock price above the long call but below the short call so that the long call can be maximally valuable while the short call is worthless.

If I short a call spread, I want the spread to be worthless at expiration. At what point can I maximize the above conditions?

Well, I can’t have a worthless call spread at expiration if either call has value, so I need both to be worthless.

A call will be worthless if the stock price < call strike at expiration.

So in the case of a short call spread, I need the stock price to be below both strikes for both options to be worthless at expiration.

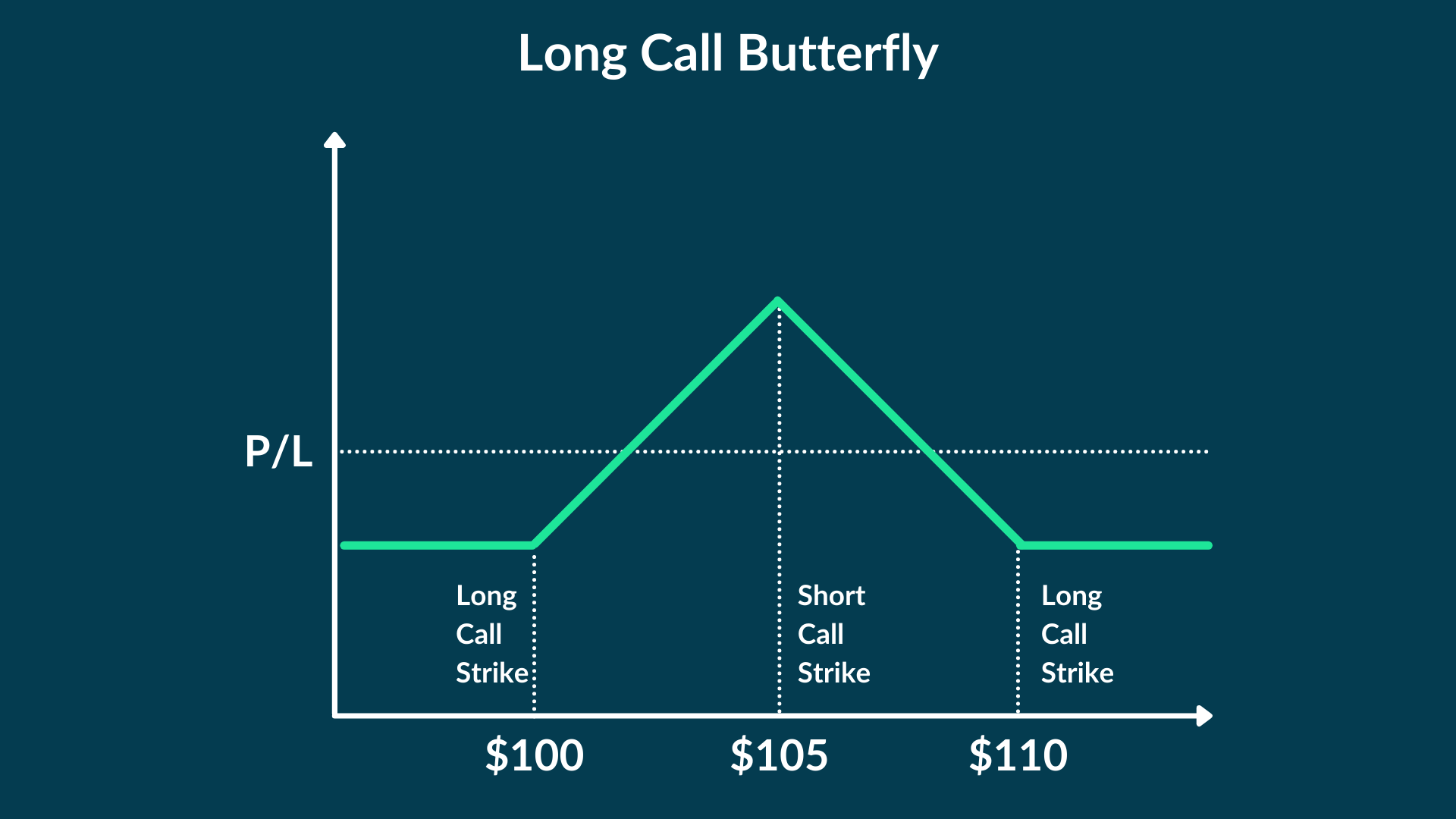

Long Call Butterfly

What about more complex options strategies like a long call butterfly?

A long call butterfly consists of:

Buying 1x call, shorting 2x calls at a higher strike price, Buying 1x call at an even higher strike price.

Example: Buy 1x 100 call, short 2x 105 calls, buy 1x 110 call.

Long Call: I want the call to be as valuable as possible at expiration.

Short Call: I want the call to be worthless at expiration.

Since I am buying a call butterfly, I want the butterfly to be valuable at expiration.

At what price can I maximize the value of the long calls while minimizing the value of the short calls?

I would approach this by going through each strike price and assessing the expiration outcomes:

1) Stock @ $100

100 Call => $0

105 Calls => $0

110 Call => $0

2) Stock @ $105

100 Call => $5

105 Calls => $0

110 Call => $0

3) Stock @ $110

100 Call => $10

105 Calls => $5 each ($10 total for 2x contracts).

110 Call => $0

The only scenario that satisfies the question “At what price can I maximize the value of the long calls while minimizing the value of the short calls?” is Scenario #2 (stock @ $105).

In scenario #1 (stock @ $100), all options expire worthless and we lose the premium paid for the butterfly.

In scenario #3, the 100 call I own is worth $10, but the short 105 calls are worth a total of $10 ($5/each x 2). The position is worth $0 and I lose the premium paid for the butterfly.

Using mental frameworks like these allows us to better understand options strategies without memorizing formulas. We were able to walk through the optimal scenario for a few strategies in the previous scenarios without using formulas.

The way to truly master options trading (or anything) is to always ask “why?”

Memorizing a formula is not understanding. Whenever you’re learning something new, seek to understand the why.

Whenever you’re listening to somebody talk about something and they’re able to articulate it well, it’s because they’ve sat with the why for so long that they eventually unlocked a deep understanding of the subject.

“It's not that I'm so smart, it's just that I stay with problems longer.”

-Albert Einstein

I encourage you all to spend time sitting with new concepts (while learning anything). It takes time. I go through the process all the time.

By trying to understand strategies and concepts as we did in this post, you’ll learn options trading on a deeper level than you will by memorizing formulas.

A great way to test your understanding is to write about it. Writing about options to teach others has undoubtedly helped me learn faster because I had to sit with the ideas long enough to put them into simple terms. If I find it hard to write about something clearly, then it’s a sign that I haven’t yet grasped the concept and need to keep thinking about it.

Did you find this helpful? Let me know!

Enjoy your weekend!

-Chris

Excelent and easy to understand. Thanks

Hi, Chris,

Thanks for the explanation. Will you be sharing also for put options? I'm interested in sell put as you can collect premiums for doing that. Thanks